What credit score is required for tire financing?

What credit score is required for tire financing?

Most car loan borrowers maintain credit scores of 661 or higher. When it comes to tire financing, many shoppers worry about meeting minimum credit requirements. Here's the reality - no set credit score determines your ability to finance tires.

At Performance Plus Tire, we work with customers across all credit ranges. Whether your score sits in the 600-630 range or below, tire financing options remain available. Lower credit scores typically result in higher interest rates, but numerous retailers provide specialized tire credit programs for challenging credit situations. We offer multiple financing solutions designed to help customers rebuild their credit while getting the tires they need.

Our guide covers everything you need to know about tire financing credit requirements, shows you the best options for different credit situations, and provides proven strategies to maximize your approval chances regardless of your current score.

What Credit Score Ranges Mean for Tire Financing

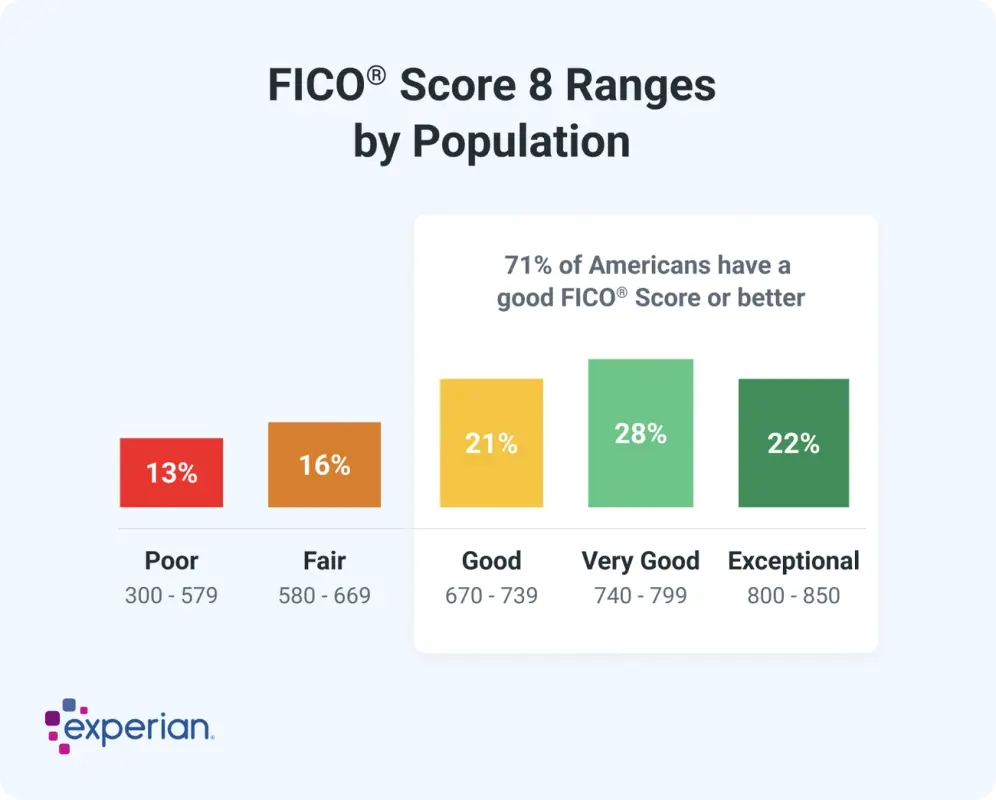

Image Source: Experian

Credit scores determine your tire financing options and interest rates. This three-digit number, ranging from 300 to 850+, helps lenders quickly evaluate your creditworthiness.

Superprime to deep subprime explained

Lenders classify borrowers into specific tiers based on credit scores. Understanding these categories helps you know what to expect:

Super-Prime (740-850+): Top-tier borrowers qualify for the best financing terms, including interest rates below 3% on auto-related loans. Experian classifies super-prime as 781-850.

Prime (680-739): Good credit borrowers still receive competitive rates, typically between 4.75-6.15% for vehicle-related purchases.

Nonprime/Near-Prime (620-679): This middle tier faces moderate interest rates around 7.55-10.85%.

Subprime (580-619): Borrowers here encounter significantly higher interest rates, approximately 11.51-16.88%.

Deep Subprime (below 580): The highest risk category faces the steepest rates, often 14.25-19.81% for auto-related financing.

How lenders view different score brackets

Most tire financing requires a minimum score of 650 for standard approval. Each lender sets their own criteria when evaluating applications.

Your credit report shows payment history, borrowing patterns, and financial discipline. Even with scores below 650, consistent on-time payments and responsible financial behavior can lead to approval.

Lenders evaluate several factors beyond your credit score:

Monthly income

Debt-to-income ratio

Payment history

Length of credit history

On-time payment history carries the most weight because it demonstrates reliability. Higher scores unlock better terms and lower interest rates for tire financing.

Remember that loan denials don't harm your credit score, though multiple applications (hard inquiries) can negatively impact it.

Best Tire Financing Options for Low Credit

Image Source: Commercial Tire

When you need tires but have credit challenges, several retailers provide financing solutions designed for your situation. We've compiled the most accessible options that work for different credit profiles.

Firestone Credit Card Approval Odds

The Firestone Credit Card typically requires a credit score of at least 640 for approval. While this sits in the fair credit range, they evaluate multiple factors beyond your score. Your income, existing debt load, number of open accounts, recent inquiries, employment status, and housing situation all play a role in their decision.

The card provides several key benefits for credit rebuilding:

No annual fees

6-month promotional financing on purchases of $149 or more

Low monthly payments that fit your budget

Keep in mind the card carries a 34.99% APR as of January 2025. Paying off promotional balances before the 6-month period expires becomes essential to avoid accumulated interest charges.

Les Schwab: Easy Approval and 0% Offers

Les Schwab offers straightforward credit options with customer-friendly policies. Their application process delivers immediate results with basic information.

They provide three distinct payment plans:

Retail Payment Plan: Most popular choice where monthly payments decrease as your balance reduces

Equal Pay: Fixed monthly payments at 5% of your highest balance

90-Days Same as Cash: No interest charges when paid in full within 90 days

For example, a $500 tire purchase with Equal Pay requires just $25 monthly payments until completion.

Tire Credit Cards for Bad Credit Shoppers

Credit First National Association partners with thousands of automotive retailers nationwide, offering credit cards specifically designed for tire purchases. Their application process moves quickly with flexible criteria to help qualify customers with low scores or limited credit history.

Many retailers provide specialized financing programs. Performance Plus Tire offers financing options for various credit situations, helping you get the tires you need regardless of credit challenges.

These automotive private label credit cards can boost your credit score when used responsibly, creating dual benefits - getting necessary tires while improving your financial standing.

Tips to Improve Approval Chances

Getting tire financing with credit challenges requires the right preparation. Smart preparation can significantly boost your approval odds even with a lower credit score.

Bring proof of income and address

Lenders need verification of your financial stability before approving any financing. Come prepared with:

Pay stubs from the last month

W-2s or tax returns

Bank statements showing consistent income

For address verification, bring utility bills, bank statements, or a lease agreement. These documents confirm your identity and affect the sales tax calculated on your purchase.

Use collateral or make a down payment

A substantial down payment reduces the amount you need to finance. Lenders view customers who provide down payments as lower risk applicants.

Financial experts recommend down payments of at least 20% for new purchases or 10% for used items. Putting money down leads to better loan terms and lower interest rates. Increasing your down payment by just $1,000 can decrease your monthly payment by approximately $20.

Avoid hard inquiries when possible

Multiple credit applications can damage your score. Look for lenders offering "soft pull" preapprovals that won't impact your credit. Many tire retailers like Performance Plus Tire offer payment plans that look beyond traditional credit scores, requiring just basic identification and income verification.

What to Expect After Approval

Image Source: Document

Once you receive tire financing approval, understanding your agreement terms becomes essential. Different companies structure their financing programs based on your credit profile and specific needs.

Understanding Your Repayment Terms

Review your financing agreement carefully before signing. Tire financing comes in two main forms: traditional loans or lease-to-own agreements. Traditional financing offers APRs ranging from 0% to 29.99% based on your credit quality. Payment terms usually extend from 3 to 48 months. Lease-to-own programs work differently - you make regular payments until completing the contract, though these typically cost more than cash purchases.

Early Buyout Options and Fees

Many tire financing programs include early buyout windows lasting 90-101 days that can save you significant money. These "same-as-cash" promotions eliminate interest charges when you pay off your balance during the promotional period. Programs like Bread Pay don't charge origination fees or prepayment penalties. We recommend making larger payments than required to complete your payoff before the early buyout period ends.

How Tire Financing Can Affect Your Credit

Regular tire financing payments can actually improve your credit score over time. This makes tire financing an excellent tool for credit rebuilding, particularly since many applications use soft credit checks that don't impact your score. Successfully completing your tire financing demonstrates responsible financial behavior to credit bureaus, potentially opening better borrowing opportunities in the future.

Conclusion

Tire financing works for all credit levels. While many lenders prefer scores around 650 or higher, options exist for every credit situation.

Your credit score affects your interest rate more than your approval chances. Understanding your credit range helps you prepare for the terms you'll receive. Firestone, Les Schwab, and specialized tire credit cards provide accessible financing solutions for different credit profiles.

Preparation makes the difference between approval and rejection. Proper documentation, down payments, and avoiding multiple credit inquiries improve your success rate. Review your agreement terms carefully - early buyout options can save you significant money.

Responsible tire financing strengthens your credit profile over time. Consistent payments demonstrate financial reliability to credit bureaus while getting you the tires you need. This creates benefits for both immediate transportation needs and long-term financial health.

Getting tire financing might feel challenging with credit concerns. Armed with knowledge about requirements, options, and strategies, you can confidently approach tire retailers knowing solutions exist for your situation.

Ready to get the tires you need? Visit Performance Plus Tire today and explore financing options that work for your credit profile. Our expert team is ready to help you find the perfect solution for your vehicle and budget.

Key Takeaways

Understanding tire financing options can help you secure the tires you need regardless of your credit situation, with proper preparation being key to approval success.

• No minimum credit score required: While lenders prefer 650+, tire financing is available for all credit levels with varying interest rates (0-29.99% APR).

• Multiple financing options exist: Firestone Credit Card (640+ score), Les Schwab's flexible plans, and specialized tire credit cards cater to different credit situations.

• Preparation improves approval odds: Bring income proof, consider down payments (10-20%), and avoid multiple hard credit inquiries to maximize chances.

• Early payoff saves money: Most programs offer 90-day same-as-cash options that eliminate interest charges if paid within the promotional period.

• Builds credit when managed well: Consistent tire financing payments can improve your credit score over time while meeting immediate transportation needs.

Remember that tire financing serves dual purposes - getting necessary tires now while potentially strengthening your credit profile for future borrowing opportunities.

FAQs

Q1. What credit score do I need for tire financing? There's no set minimum credit score required for tire financing. While many lenders prefer scores of 650 or higher, options exist for all credit levels. Your score primarily affects the interest rate you'll receive rather than approval itself.

Q2. Are there tire financing options for bad credit? Yes, several options cater to those with less-than-perfect credit. Specialized tire credit cards, Les Schwab's flexible plans, and some retailers' in-house financing programs are designed to help those with lower credit scores get the tires they need.

Q3. How can I improve my chances of getting approved for tire financing? To increase your approval odds, bring proof of income and address, consider making a down payment (10-20% is recommended), and avoid multiple hard credit inquiries. These steps demonstrate financial stability and reduce the lender's perceived risk.

Q4. What should I know about repayment terms for tire financing? Repayment terms typically range from 3 to 48 months, with APRs varying from 0% to 29.99% based on your credit profile. Many programs offer early buyout options, such as 90-day same-as-cash deals, which can save you money if paid off within the promotional period.

Q5. Can tire financing help improve my credit score? Yes, responsible management of tire financing can potentially improve your credit score over time. Making consistent, on-time payments demonstrates financial reliability to credit bureaus, which can positively impact your credit profile.

Comments

Post a Comment